I’ve worked with many business owners who tossed out boxes of documents, only to face an IRS audit years later. “Why didn’t anyone tell me?” they’d ask. The IRS clearly publishes how long you need to keep business records, but most people don’t read the fine print. Through consulting with CPAs and business owners navigating audits, I’ve learned that understanding how long to keep business records is one of the most important yet overlooked aspects of running a business. Let me walk you through exactly how long you have to keep business records so you know what to save, what to discard, and what could protect you if trouble arises.

Why Keeping Business Records Matters

Before we dive into timelines, understand why this matters. Business record retention isn’t just bureaucratic busywork. It’s essential for several reasons.

Legal Protection

If the IRS audits you, your records will be your defence. They prove your income. They prove your deductions. They prove you followed the rules. Without them, you’re vulnerable. The IRS can assess additional taxes, penalties, and interest.

Financial Management

You can’t manage what you don’t measure. Good records let you understand your business finances. Cash flow. Profitability. Where money comes from. Where it goes. These insights drive business decisions.

Loan and Investment Requirements

When you apply for a loan or seek investment, lenders and investors ask for financial records. Three years of tax returns and supporting documents is standard. Without them, you can’t prove your business’s health.

Business Sale

If you eventually sell your business, buyers want to see historical financial records. Organized, complete records make your business more valuable and easier to sell.

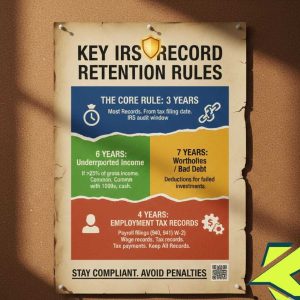

The Core Rule: 3 Years for Most Records

Here’s the foundational rule from the IRS. Keep business records for at least 3 years from the date you file your tax return.

This 3-year period aligns with the statute of limitations. The IRS generally has 3 years from your filing date to audit your return and assess additional taxes. If they can’t verify your income and deductions within that time, they typically can’t go after you.

But—and this is important—there are significant exceptions. Let’s explore them.

The Major Exceptions to the 3-Year Rule

These exceptions extend your record retention obligations considerably.

6 Years: Underreported Income

If you underreport income by more than 25% of your gross income shown on your return, keep records for 6 years.

Example: Your return shows $100,000 in income. You failed to report $26,000 of income (26% underreport). The IRS now has 6 years to audit you. Keep all supporting documents for 6 years.

This is common when people forget to include 1099 income or misreport cash sales.

7 Years: Worthless Securities or Bad Debt

If you claim a deduction for worthless securities or bad debt, keep records for 7 years.

Example: You invested $10,000 in a company that went bankrupt. You claim a bad debt deduction. Keep all records of that investment for 7 years.

4 Years: Employment Tax Records

If you have employees, you must keep payroll tax records for at least 4 years after the tax becomes due or is paid, whichever is later.

This includes:

- Payroll tax filings (940, 941)

- W-2s and W-3s

- Employee wage records

- Tax payment documentation

Employment tax violations carry significant penalties, so the IRS takes these seriously.

Indefinitely: Fraudulent Returns or No Return Filed

If you file a fraudulent return or don’t file a return at all, there’s no statute of limitations. Keep records indefinitely.

This also applies to failures to file required foreign financial reports.

What Specific Records to Keep and For How Long

Let me break this down by document type. This is where details matter.

Tax Returns and Supporting Documents

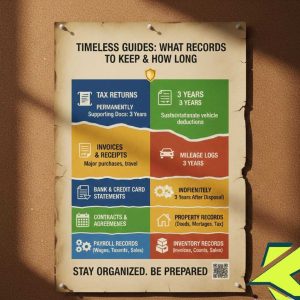

Keep copies of your filed tax returns permanently. These prove you filed and what you claimed. Supporting documents (income statements, deduction receipts, expense documentation) keep for at least 3 years.

Bank Statements and Cancelled Checks

Keep for 3 years minimum. These prove your income and expenses. They’re crucial for substantiating deductions.

Invoices and Receipt

Keep for 3 years. Receipts prove the business expenses you deducted. The IRS specifically requires you to keep receipts for major purchases and travel expenses.

Mileage Logs

Keep for 3 years. Mileage logs substantiate vehicle deductions. The IRS often audits these because people claim inflated mileage.

Credit Card Statements

Keep for 3 years. These documents business charges and prove payment.

Payroll Records

Keep for 4 years if you have employees. These include salary, wages, payroll taxes paid, and tax withholdings.

Asset and Depreciation Records

Keep for 3 years after you dispose of the asset. This includes equipment purchases, depreciation schedules, and business equipment information. These are critical because depreciation affects multiple years’ tax returns.

Property Records

Keep indefinitely. Real estate deeds, mortgage documents, and property tax records should be kept for the life of your ownership plus several years after sale.

Contracts and Agreements

Keep for 3 years plus the contract duration. Business contracts, leases, and vendor agreements document your business relationships and obligations.

Inventory Records

Keep for 3 years. Purchase invoices, inventory counts, and sales records prove your cost of goods sold calculations.

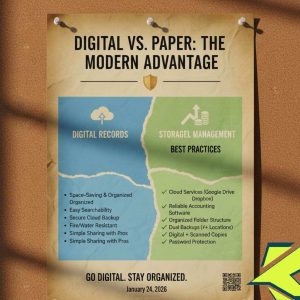

Digital vs. Paper Records

The IRS accepts both digital and paper records. Digital records are perfectly fine as long as they’re accurate, legible, and easily accessible.

Advantages of Digital Records

- Takes up minimal space

- Easy to organize and search

- Can be backed up to multiple locations

- Less likely to be destroyed by fire or water

- Easier to share with accountants and tax professionals

Storage Options

Cloud storage services like Google Drive, Dropbox, or OneDrive work fine. Accounting software that automatically stores records works well. The key is reliability and accessibility.

Best Practices

- Maintain organized folder structure

- Back up records to at least two locations

- Keep both digital and scanned copies for important documents

- Use password protection for sensitive financial information

What the IRS Can Request Beyond Your Return Period

Here’s something many people don’t know. While the IRS has a 3-year statute of limitations, they can request to see records going back further if they identify issues.

If they find a substantial error (usually defined as more than 25% underreporting), they can request records going back up to 6 years. Some estimates put IRS audit authority at up to 10 years if they suspect deliberate fraud.

This is why keeping records longer than 3 years provides safety. Conservative practice is to keep records for 7 years for this reason.

When You Can Safely Discard Records

Once your retention period is over, can you discard everything? Before discarding, consider:

Insurance Company Requirements

Your insurance company may require longer retention. Check your policy. Property insurance, liability insurance, and other policies might require 5-7 years of records.

Creditor Requirements

Creditors may require longer retention, especially if you owe money or have active loans. Check with them before discarding.

State Requirements

Some states have different recordkeeping requirements than the IRS. Sales tax records, employment records, and business licensing documents may have state-specific retention periods.

Non-Tax Business Reasons

Beyond taxes, consider keeping records if:

- You might sell your business (buyers want 3+ years of financials)

- You might apply for loans (lenders want 3+ years of history)

- The record documents ongoing obligations

- The record documents asset ownership or depreciation

Safe Disposal

When you do discard records, shred them or use a document destruction service. Don’t throw sensitive financial documents in the trash. Identity thieves target business records containing tax identification numbers, bank account information, and employee data.

Connecting Your Records to Your Business Success

Proper business record keeping is foundational to everything else you’re doing in your business.

When you understand how business tax write-offs work, you’re learning what deductions to claim. But those deductions mean nothing without supporting documentation. Deductible business expenses need receipts, invoices, and proof of payment. Keep these records meticulously for at least 3 years. If you claim Section 179 depreciation on business equipment, keep depreciation schedules and purchase documentation for the asset’s life plus 3 years.

If you’re building your Google Business Profile, we have a guide on how to access your Google Business Profile. Your profile’s accuracy depends on consistent, documented business operations. Good records ensure you’re reporting accurate information.

If you’re using Pinterest to market your business, we have a guide on how to use Pinterest for business. Pinterest advertising costs are deductible business expenses. Keep documentation of all advertising spending.

If you operate a taxi business, we have a guide on how to start a taxi business. Taxi businesses require meticulous fuel, maintenance, and mileage records. Keep these for at least 3 years.

If you run a coffee shop business, we have a guide on how to start a coffee shop business. Restaurants must keep detailed inventory, sales, and expense records for accounting and tax purposes.

If you operate a home staging business, we have a guide on how to start a home staging business. Inventory purchase receipts, mileage logs for client visits, and expense documentation all need retention for 3 years.

If you run a virtual assistant business, we have a guide on how to start a virtual assistant business. Client invoices, time tracking records, and payment documentation should be kept for 3 years.

When you understand how to value your business, we have a guide on how to calculate business valuation. Buyers want to see historical financial records. Organized, documented records increase your business’s value significantly.

Common Record-Keeping Mistakes

Learn from others’ failures.

Throwing Away Records Too Soon

Many business owners discard records after one year. This is dangerous. You need 3 years minimum, longer for certain documents.

Keeping No Records At All

Some self-employed people operate on cash with no documentation. If audited, they have no proof of income or expenses. They lose nearly every deduction. Don’t do this.

Disorganized Records

Shoeboxes full of receipts. Crumpled bills stuffed in drawers. Digital files scattered across multiple devices. Poor organization makes it hard to substantiate deductions and difficult to find documents if audited.

Inconsistent Records

Records that don’t match between systems. Your accounting software shows one number, your bank shows another. The IRS notices inconsistencies immediately.

No Support for Claimed Deductions

You can’t prove you spent money on a deduction you claimed. The IRS denies it. Keep receipts and proof of payment for everything you deduct.

Professional Help and Record Organization

If recordkeeping overwhelms you, get help.

A CPA can set up a system, review your records for compliance, and advise on what to keep. Cost ($500 to $2,000 annually) is well worth the peace of mind and tax savings.

Accounting software like QuickBooks, FreshBooks, or Wave automatically tracks and organizes records. Many integrate with your bank, automatically categorizing transactions.

Document management systems keep digital records organized and easily searchable.

The Bottom Line

Keep business records for at least 3 years. But understand the exceptions. Keep employment records for 4 years. Keep records documenting worthless securities or bad debt for 7 years. Keep records related to underreported income for 6 years. Keep permanent records of tax returns and major business transactions indefinitely.

Don’t guess. Don’t throw things away recklessly. When in doubt, keep the document.

Organized, complete business records protect you in audits, help you manage your finances, and make your business more valuable if you ever sell.

Start today. Implement a system. Organize your records. Back them up. Keep them safe.

FAQs:

Q: Can I destroy records after the IRS statute of limitations expires?

A: Yes, generally after 3 years (or longer for certain records). But check with insurance companies, creditors, and state requirements first. Some require longer retention.

Q: The IRS audited me for a prior year. How long should I keep those records?

A: Keep audit-related records indefinitely. They may reference those years in future audits. Having them protects you.

Q: Can I store business records digitally?

A: Absolutely. Digital records are acceptable as long as they’re accurate, legible, and easily accessible. Backup to multiple locations for safety.

Q: What if I lose my records in a fire or flood?

A: Contact the IRS immediately. You can request an extension and may be able to reconstruct records or provide alternative documentation. Don’t wait to report this.

Q: Do I need to keep physical copies or can everything be digital?

A: Everything can be digital if you maintain a backup system and can retrieve documents quickly. Many people keep both for critical documents like tax returns.

Q: How do I know if the IRS is going to audit me?

A: You don’t until you receive a notice. But maintaining complete, organized records for 7 years is the safest approach. This protects you regardless.

Q: Can my accountant keep my records instead of me?

A: Yes, but get a written agreement about retention periods and retrieval procedures. You’re ultimately responsible for having records available if audited.

Hi, I am the founder of KlickTrust. I’m a digital strategist and builder with a deep passion for creating systems that help people build faster online. I started KlickTrust to save creators, freelancers, and entrepreneurs from wasting months starting from scratch by giving them access to practical, ready-to-use digital tools, templates, and automation systems that actually work in the real world.

At KlickTrust, I focus on speed, trust, and empowerment, so you can launch, grow, and scale with confidence.