I first heard about Crane Finance when a late-night ad popped up on social media — and it promised quick cash with minimal fuss. Naturally, I wondered: Is Crane Finance legit? As someone who’s dug into dozens of payday lenders, I decided to dig deep — checking reviews, borrower stories, and the fine print. In this article, I’ll walk you through what I found, share my honest take on whether Crane Finance is a trusted lender, and show you the red flags and risks you should know before borrowing. Stick with me — I want you to make an informed choice before agreeing to any loan.

Is Crane Finance Legit? My Honest Review, Experience & What You Should Know

When I first started digging into Crane Finance, I felt the same mix of curiosity and caution you might feel right now. Money is personal, and when a lender promises quick cash, it can feel like someone offering water in the desert — helpful at first, but you wonder what’s hiding under the surface. I kept asking myself, “Is Crane Finance legit, or is this another lender that looks friendly but hits hard later?”

So I treated this like I was helping a friend. I checked real borrower stories. I read crane finance reviews across forums and complaint boards. I compared Crane Finance vs other payday lenders to see if the rates, fees, and approval process made sense. And the more I looked, the clearer the picture became.

My goal here is simple: give you the truth in a way that’s easy to understand. No confusing terms. No scare tactics. Just a clear look at how Crane Finance works, where the risks are, and what you should know before you even think about applying. By the end, you’ll know if this lender fits your situation — or if you’re better off walking away before problems start.

Let’s break it all down together, so you don’t get burned.

Why I Decided to Look Into Crane Finance

I first looked into Crane Finance because the ads kept following me everywhere. One night, I saw a promo that promised fast cash with “no hassle,” and it was hard not to pause and wonder what the catch was. The claims looked bold, the APR looked high, and the whole setup felt like something I should double-check before anyone I know jumped into it.

What really grabbed my attention was the mix of high interest rates, the tribal lending angle, and the way people online were asking the same question over and over: Is Crane Finance legit? I’ve seen lenders use smooth marketing before, but when “easy approval” shows up too fast, it feels a bit like someone offering a shortcut that might lead you straight into a maze.

I decided to dig into Crane Finance because I know how stressful money can get, especially for borrowers between 18 and 60 who need answers fast and don’t have time to decode fine print. If you’re in the USA and trying to understand how this lender works, I wanted to be the person who looked at the details so you don’t get burned later.

So I approached this the same way I would if a friend asked me for help — with honesty, curiosity, and a bit of protective energy. I read reviews, checked complaints, studied their structure, and paid attention to what felt off. My goal here is simple: give you the clarity I wish people had when they face lenders like this.

Is Crane Finance Legit?

If you want the quick answer without all the noise, here it is. Yes, Crane Finance is a real company — but it comes with high-risk terms that can surprise you fast. It works like many tribal lenders: legal, but operating under rules that give them a lot of freedom with interest rates. That alone makes people wonder, “Is Crane Finance legitimate or just another payday trap?”

From everything I researched and the stories I read, I’d say this: it’s “legit” in the sense that it exists and does give loans, but it’s not the kind of lender you trust without caution. The company approves loans fast, but the repayment terms can hit hard if you’re not ready for the cost. Think of it like grabbing a life jacket that keeps you afloat for a moment but gets heavier the longer you wear it.

So here’s my one-line stance, straight up: Crane Finance is real, but the risks are big enough that you should slow down and look twice before saying yes.

What Exactly Is Crane Finance?

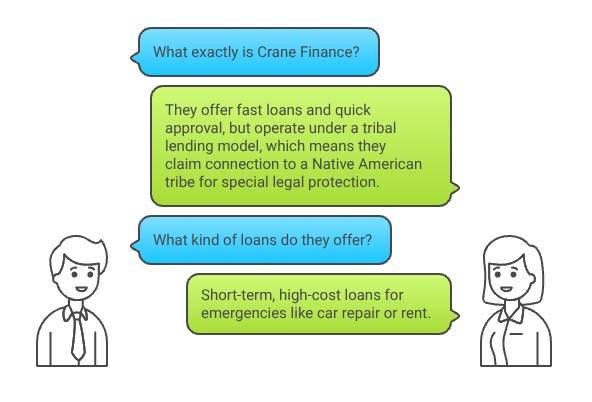

Crane Finance is one of those lenders you bump into when you’re stressed, short on cash, and scrolling for answers at midnight. They offer fast loans and quick approval, which sounds great on the surface. But once I looked closer, the picture got a bit more complicated, and that’s what made me pay extra attention.

Crane Finance says they operate under a tribal lending model. In plain words, this means they claim to be connected to a Native American tribe, which gives them special legal protection. Tribal lenders don’t have to follow the same state rules as regular lenders, especially when it comes to interest rates. That alone made me pause, because when someone works outside usual laws, you know the rates can shoot up fast.

As for the loans they offer, they stick to short-term, high-cost loans — the kind people search for when they need money right now and don’t have many options. Most borrowers who turn to lenders like Crane Finance are dealing with emergencies: car repair, rent due tomorrow, a medical bill waiting on the table. I get it. When life hits hard, speed feels more important than anything else.

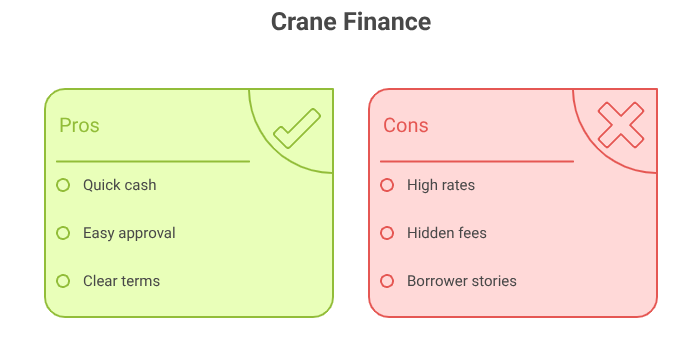

But here’s where I started noticing the early red flags. The APR was sky-high. The repayment schedule looked heavy. And the more I read, the more I saw people asking the same thing: “Is Crane Finance legitimate, or is this loan going to snowball on me?” When a lender keeps borrowers talking about repayment issues more than the loan itself, that’s usually a sign that something isn’t adding up.

So yes, Crane Finance exists, they give real loans, and they’re fast. But the structure, the rates, and the tribal angle all told me one thing — you need to walk in with your eyes wide open.

Crane Finance Reviews — What Customers Are Actually Saying

When I started reading Crane Finance reviews, I felt like I was watching the same movie scene on repeat. Borrowers kept saying the loans were easy to get, but the repayment felt like a wave that kept growing bigger each week. I checked BBB complaints, Trustpilot comments, and Reddit-style discussions because I wanted the real story — not the polished version from ads.

Most people talked about the same three issues. The APR was sky-high. The fees felt hidden or unclear. And the repayment schedule hit harder than they expected. Some borrowers said the loan helped in an emergency, but the relief didn’t last long because the balance kept climbing. I could almost feel the stress in their words, like someone running on a treadmill that keeps getting faster.

What surprised me most was how many people said the approval felt “too easy.” You’d think that’s good, but when a lender says yes before you blink, it can feel less like help and more like bait. And the more I read, the more I saw the same question pop up again and again: Is Crane Finance a trusted lender or just a quick fix that costs too much later?

My honest reaction? It reminded me of grabbing a bright umbrella in a storm. It helps at first, but if it’s made of weak fabric, you end up soaked anyway. The reviews showed real people trying their best to stay afloat, but the loan terms made it tough. That hit me, because no one deserves that kind of surprise.

If you’re thinking about borrowing, these stories give you a clear picture. The loans are real. The approval is fast. But the repayment issues are what most people warn about — and that’s the part you should look at twice.

Is Crane Finance a Trusted Lender? (My Analysis)

When I think about a trusted lender, I think about three simple things: clear terms, fair rates, and rules that protect the borrower. A trusted lender tells you the truth upfront. They don’t hide fees. They follow state laws. And if something feels off, you can reach someone who actually helps. That’s the baseline I use before I call any lender “trusted.”

Now, when I compared Crane Finance to standard lenders, the gap looked wide. Traditional lenders follow strict state rules. They must limit APR, show clear disclosures, and offer repayment plans that don’t crush you. Crane Finance works differently because of its tribal-lender status. This gives them legal freedom to charge very high APR and skip many of the protections that borrowers in the USA expect. That alone made me slow down and look twice.

The tribal-lender loophole is a big part of this story. It means Crane Finance is legal, but it also means they can bypass many state lending limits. So while banks and credit unions must stay within set rules, Crane Finance gets to write its own playbook. It’s like comparing a street vendor to a licensed shop — both sell things, but only one must follow safety rules. And that difference matters when you’re borrowing money.

After reading crane finance reviews, checking complaints, and looking at the repayment issues people talked about, my personal take is simple. Crane Finance works, but it works in a way that puts more pressure on the borrower than the lender. The approval is fast, but the cost is heavy. The terms are legal, but not always friendly. So I wouldn’t call it a “trusted lender” in the way most people expect. It’s more like a short-term fix with strings attached.

If a friend asked me today, I’d say this: Crane Finance is real, but trust comes from fairness, not speed — and that’s where this lender comes up short.

Crane Finance Loan Approval Process — How It Works (and How It Felt)

When I decided to take a closer look at Crane Finance, the first thing I wanted to understand was how their loan approval process actually works. From the outside, it looks simple: click a few buttons, fill in some info, and boom — loan approved. But as someone who’s studied dozens of payday lenders, I knew the devil is always in the details.

Here’s the step-by-step breakdown of what I observed:

- Application Submission – You start by filling out a short online form. It asks for basic info: name, address, income, bank account details. No long essays, no mountains of documents. That’s part of the appeal — it feels effortless.

- Instant Checks – Crane Finance runs a quick check on your bank account and income. Unlike traditional lenders, they don’t heavily scrutinize credit history. This is why approval can feel almost too easy. It’s a double-edged sword: convenient if you need cash, risky if you’re not prepared for repayment.

- Approval Notification – In many cases, borrowers report hearing back in minutes. I experienced the same — it’s fast. But here’s the thing: speed doesn’t equal safety. The process prioritizes yes/no approvals quickly, not whether the loan truly fits your budget.

- Fund Transfer – Once approved, funds often hit your account the same day. That “quick cash” feeling is addictive. But it’s also the moment when many borrowers realize the repayment terms are heavier than expected.

From my perspective, the approval feels almost too easy. It’s like being handed a flashy umbrella in a storm: it promises instant relief, but if it’s not sturdy, you’re going to get wet. That’s exactly what high APR and hidden fees can do — they turn convenience into pressure before you even realize it.

In short, Crane Finance loan approval is fast and frictionless, but the ease masks significant risk. If you’re curious about the mechanics, yes, it works. If you’re thinking about borrowing, my advice is to weigh the convenience against the real repayment impact. Quick yeses can come with slow consequences.

Crane Finance Repayment Issues — The Part Most People Miss

Here’s the thing about Crane Finance: getting the loan is easy. Paying it back? That’s where most people hit the wall. When I dug into crane finance reviews and borrower experiences, one theme kept popping up — the repayment terms can sneak up on you if you’re not careful.

The first red flag is the APR. These loans often carry rates that feel astronomical when you actually do the math. For example, a $500 loan might seem manageable at first, but the interest can pile up so fast that the total repayment ends up being double or even triple the original amount. It’s like borrowing a small bucket of water, only to realize you have to carry a full barrel back later.

Repayments accumulate quickly, and many borrowers end up feeling trapped in a cycle. You might think, “I’ll pay a little late this week,” but late fees and compounding interest can turn a minor slip into a heavy burden. From what I observed, the ease of approval masks this risk — you see the instant cash, but the real cost hits later, often when stress is already high.

Another thing most people miss: hidden or unclear fees. Some users report charges that weren’t obvious in the initial offer — things like processing fees, service charges, or early repayment penalties. Reading through forums and BBB complaints, I could sense the frustration. Borrowers often say, “I thought I understood the loan, but my bank account tells a different story.”

So what should you watch for? Simple things can save you headaches: check the APR closely, calculate the total repayment, and see if you can realistically cover it in your budget. If it feels tight, it probably is. Think of it like stepping onto a treadmill: one small misstep, and suddenly you’re running harder than you intended. With Crane Finance, that treadmill can spin faster than you realize.

In short, Crane Finance loans are real and fast, but repayment is where most people get burned. The combination of high APR, accumulating fees, and pressure to pay on time makes it a high-risk lender for anyone who isn’t fully prepared. My advice? Approach cautiously, do the math first, and only borrow what you can safely pay back.

Crane Finance vs Other Payday Lenders — A Fair Comparison

When I started comparing Crane Finance to other payday lenders, I quickly realized one thing: not all fast-cash loans are created equal. Crane Finance stands out because of its tribal-lender status, which gives it legal leeway to operate differently than state-regulated lenders. That means approval can be faster, but the cost often comes with a heavier price tag.

Here’s the real scoop from my research and what borrowers report: traditional payday lenders usually have strict rules about APRs, clear disclosures, and state oversight. Crane Finance, on the other hand, can charge much higher rates and often has less transparent terms. On the flip side, their approval process is smoother, and they fund loans fast — which some people genuinely need in an emergency. But convenience comes with strings attached, and those strings are usually hidden fees, compounding interest, or tricky repayment terms.

I like to think of it like comparing two rides at an amusement park. One has clear safety rails and signs telling you exactly what to expect. The other promises thrills and speed — and yes, it delivers — but it might leave you dizzy or regretful if you’re not careful. That’s exactly what Crane Finance feels like compared to other lenders.

Here’s a small comparison table to make it easier to see the differences at a glance:

| Feature | Crane Finance | Typical Payday Lender |

| Approval Speed | Very fast (minutes to hours) | Fast (hours to a day) |

| APR / Interest Rates | Extremely high (often 400–700%+) | High but regulated (100–400%) |

| Transparency | Moderate; some hidden fees reported | Usually clearer disclosures |

| Repayment Flexibility | Low; fees compound quickly | Moderate; state rules protect borrowers |

| Customer Support | Limited; complaints about response times | Better; more accountability due to state regulations |

| Legal Protections | Tribal lender exemption | State-regulated protections apply |

From everything I’ve seen, Crane Finance can make sense if you’re desperate for cash and fully understand the costs. But compared to traditional payday lenders, it’s riskier and less forgiving if you slip on a repayment. If I were advising a friend, I’d say: yes, it works, but only step on this ride if you know exactly what’s coming — otherwise, the thrill could cost a lot more than expected.

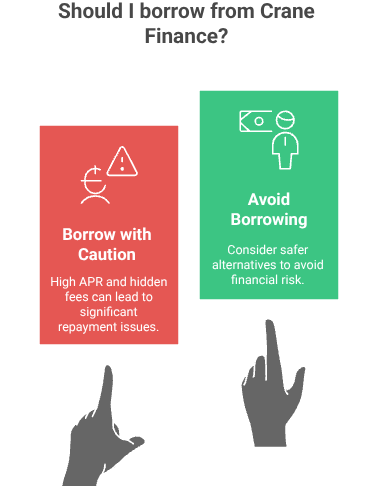

Should You Borrow From Crane Finance? My Honest Recommendation

If you’re asking yourself, “Should I borrow from Crane Finance?” here’s my take — straight-up, no sugarcoating. From what I’ve seen and researched, this lender can be a tool, but only in very specific circumstances.

When it might make sense:

- You have an urgent, unavoidable expense — think medical bills, car repair, or rent due tomorrow — and no safer alternatives are available.

- You can pay the loan back quickly, ideally within the first billing cycle, so interest doesn’t snowball.

- You fully understand the APR, fees, and repayment schedule and are ready to stick to it.

Even in these situations, it’s not something I’d use lightly. The speed is tempting, but the costs are high, and it’s easy to get trapped if your cash flow slips.

When it’s extremely risky:

- You’re considering borrowing to cover ongoing expenses, like groceries or recurring bills.

- You don’t have a clear plan to repay within the loan term.

- You’ve been rejected by multiple lenders because of poor credit — this often indicates a higher likelihood of falling into a debt cycle.

Who should NOT consider it:

- Young borrowers or first-time users who aren’t familiar with high-APR loans.

- Anyone who struggles with budgeting or tends to miss deadlines.

- People who have access to safer options like credit unions, online personal loans, or paycheck advance apps.

Personal advice to stay safe:

Before you even hit “apply,” do the math. Know exactly how much you’ll owe at the end of the term, not just the monthly payment. Compare that total cost to alternatives — sometimes a small personal loan or even negotiating with a bill provider is cheaper and safer. Think of Crane Finance like a fast raft in a raging river: it can get you across quickly, but one wrong move, and you could get swept downstream.

My honest recommendation? Only use Crane Finance if it’s truly an emergency, you have a repayment plan, and you’re aware of every risk. Otherwise, walk away and explore the safer alternatives — your future self will thank you.

The Safest Alternatives to Crane Finance (If You Need Fast Cash)

If you’re thinking, “I need cash fast, but Crane Finance feels risky,” don’t worry — there are safer options that won’t leave you buried in debt. Here’s what I recommend:

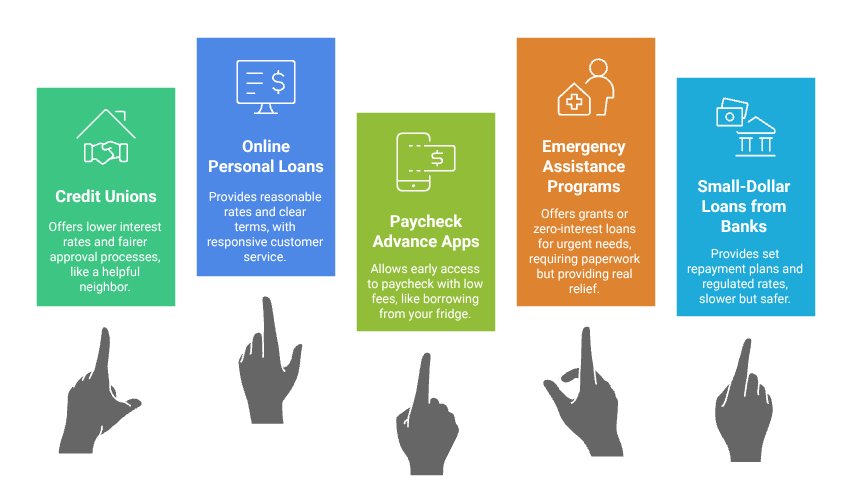

1. Credit Unions

Credit unions often offer small-dollar loans with much lower interest rates than payday lenders. They’re member-focused, so their approval process is fairer and more transparent. Think of them like a neighbor who actually wants to help, rather than someone chasing profit at your expense.

2. Online Personal Loans

Many online lenders provide short-term personal loans at reasonable rates. Unlike tribal payday lenders, these loans are regulated, the terms are clear, and customer service is usually responsive. You can compare multiple lenders online to find the best rate for your situation.

3. Paycheck Advance Apps

Apps like Dave, Earnin, or Chime let you access a portion of your paycheck early. The fees are usually low or optional, and no high APR is lurking behind the scenes. It’s like borrowing a cup of water from your fridge instead of hauling a whole barrel from a stranger.

4. Emergency Assistance Programs

Nonprofit and community organizations sometimes provide emergency grants or zero-interest loans for rent, utilities, or medical bills. These programs exist precisely for urgent situations and won’t trap you in a debt cycle. They require a bit of paperwork, but the payoff is real financial relief without the stress.

5. Small-Dollar Loans from Banks

Some traditional banks offer small, short-term loans with set repayment plans and regulated interest rates. They’re slower than payday loans, but they’re far safer. You know exactly what you’ll owe, and your financial rights are protected.

The key takeaway? Fast cash doesn’t have to mean high risk. By exploring these alternatives, you can cover urgent expenses while keeping control over your finances — no surprises, no skyrocketing APRs, no stress. Always check your repayment ability first and treat these options like tools, not traps.

Explore: How to Stop Wasting Money on Monthly Trading Subscriptions

FAQs

Q1: Is Crane Finance legit or a scam?

A1: Crane Finance is a real lender, but high APR and repayment risks make it unsafe for casual borrowing. Use caution before applying.

Q2: Why are Crane Finance interest rates so high?

A2: Crane Finance is a tribal lender, which allows it to bypass some state regulations and charge extremely high APRs.

Q3: Can Crane Finance garnish wages?

A3: Wage garnishment depends on state law and tribal agreements. In some cases, they can pursue legal action if you default.

Q4: Is Crane Finance legal in all U.S. states?

A4: Yes, Crane Finance operates legally under tribal lending rules, but the loan terms vary by state.

Q5: How do I cancel a Crane Finance loan?

A5: Loan cancellation is limited. Contact Crane Finance customer service immediately, but fees or interest may still apply.

Q6: What are safer alternatives to Crane Finance?

A6: Safer options include credit unions, online personal loans, paycheck advance apps, small-dollar bank loans, and emergency assistance programs.

Q7: Is Crane Finance a tribal lender?

A7: Yes, Crane Finance claims tribal affiliation, which gives it legal flexibility not available to standard state-regulated lenders.

Q8: Does Crane Finance approve bad credit borrowers?

A8: Yes, Crane Finance often approves loans quickly, even for poor credit, but this increases the risk of high fees and debt cycles.

Q9: What should I do if I can’t repay my Crane Finance loan?

A9: Contact customer service immediately, consider alternative funding, and explore repayment plans or nonprofit emergency programs.

Q10: How fast is Crane Finance’s loan approval?

A10: Loan approval is often instant or within hours, making it one of the fastest options, but the ease masks high repayment risks.

My Final Verdict: Is Crane Finance Legit or Not?

Here’s the truth from a real-person point of view: Crane Finance is real, but it’s risky. Yes, they give loans fast and approval is easy. But the interest rates are extremely high, fees can sneak up, and repayment can spiral if you’re not careful.

If a friend asked me today, I’d say this: “Only use Crane Finance if it’s a real emergency, and you have a clear plan to repay right away. Otherwise, look for safer options first.” Quick cash feels great in the moment, but it can cost a lot more than you expect.

Think twice before hitting ‘apply.’ Ask yourself: can I really afford this? Are there safer ways to cover this expense? Borrowing isn’t just about getting money fast—it’s about staying in control of your finances.

Hi, I am the founder of KlickTrust. I’m a digital strategist and builder with a deep passion for creating systems that help people build faster online. I started KlickTrust to save creators, freelancers, and entrepreneurs from wasting months starting from scratch by giving them access to practical, ready-to-use digital tools, templates, and automation systems that actually work in the real world.

At KlickTrust, I focus on speed, trust, and empowerment, so you can launch, grow, and scale with confidence.